Pfizer's Profit Hike: Smoke and Mirrors or Real Recovery?

Pfizer just dropped its Q3 earnings, and the headline is undeniably positive: they beat expectations and raised profit guidance. The stock even ticked up a bit. But before we pop the champagne, let's crack open the numbers and see what’s really going on.

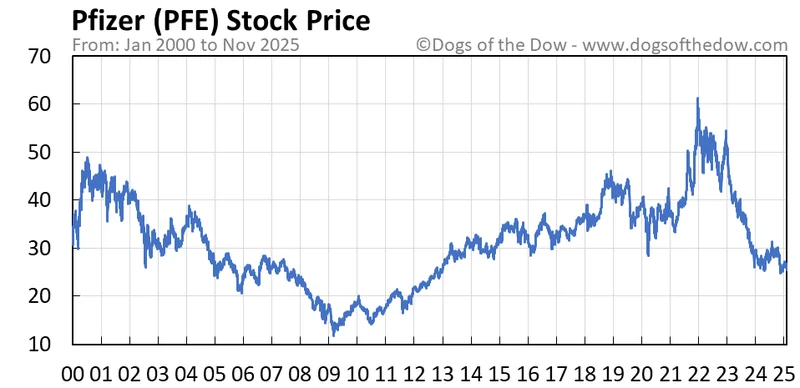

The headline EPS (earnings per share) came in at 87 cents, a solid 24 cents above expectations. Revenue also edged past estimates, landing at $16.65 billion against an expected $16.58 billion. So far, so good. But zoom out a bit, and the picture gets murkier. Revenue is actually down 6% compared to the same quarter last year. The culprit? Predictably, a drop in demand for their Covid vaccine and Paxlovid. The Covid gravy train has officially left the station.

Cost Cuts to the Rescue?

Pfizer's management is touting its cost-cutting initiatives as the key to the improved profit outlook. They're aiming for $7.7 billion in savings by the end of 2027, with $4.5 billion of that hitting by the end of 2025. That's a hefty chunk of change. But where are these cuts coming from? Are they streamlining operations, or are they simply slashing R&D (research and development) and potentially jeopardizing future innovation? The filing doesn't give us the granular detail needed to make that call. It's a classic corporate maneuver: boost short-term profits by sacrificing long-term growth. I've seen this play out dozens of times.

Speaking of long-term growth, Pfizer is pinning its hopes on new revenue streams, particularly cancer products from the Seagen acquisition (a $43 billion bet). They're also in a dogfight with Novo Nordisk over the obesity biotech Metsera. And this is the part of the report that I find genuinely puzzling.

Pfizer claims Novo Nordisk's bid for Metsera is "illusory" and violates antitrust law. They've even filed a second lawsuit. CEO Bourla is quoted as saying their belief in the Pfizer-Metsera combination is "strong and unwavering." That's all well and good, but the market seems to disagree. Metsera itself declared Novo Nordisk's bid "superior." Is Pfizer fighting for a strategic imperative, or are they simply unwilling to admit defeat in a high-stakes bidding war?

Tariffs and Trump's Shadow

The report also mentions the impact of Trump's tariffs. Pfizer expects his existing tariffs on China, Canada, and Mexico to be factored into their 2025 guidance. But the potentially bigger news is the drug pricing deal Pfizer struck with the Trump administration. In exchange for investing $70 billion to reshore domestic drug manufacturing and research facilities, Pfizer gets a three-year grace period from Trump's pharmaceutical-specific tariffs. The company expects a dilutive effect to its 2026 outlook.

CFO Dave Denton said the deal "will help ensure U.S. patients pay lower prices for prescription medicines while providing the clarity we need to focus on our business and our investment in future innovation." That sounds good in theory, but let's be real: these deals are rarely as straightforward as they seem. How much will those lower prices actually impact Pfizer's bottom line after the three-year honeymoon ends? And will that $70 billion investment truly translate into innovation, or will it be used to simply maintain the status quo? These are questions Wall Street should be asking.

A Sugar Rush, Not Sustained Growth

Pfizer's Q3 results are a mixed bag. Pfizer tops estimates, raises profit guidance even as sales fall They beat expectations, yes, but that's largely thanks to cost-cutting and a one-time charge related to a licensing agreement with 3SBio. The underlying revenue picture is still shaky, and their future growth strategy is far from certain. I'd advise investors to look beyond the headlines and dig into the details before jumping on the Pfizer bandwagon.